Sign up for Stewardship Cents Here

How to Think When the Market gets a little Crazy

If you know me, you know I love to ski. The problem is I live in Ohio. There is plenty of snow this year but not many mountains in Ohio, although one "resort" has a run called "Mt. Mansfield," all 300 vertical feet of it. My fondest memories growing up are of family ski trips; taking on challenging steep terrain with my brothers, being in spectacular mountains and the unforgettable tumbles my one brother became famous for executing. We would call them "yard sales," possibly you can figure out why. Think where all your junk gets thrown when you sell it....

The best part of our ski trips was the relationship cultivated between traveling together, skiing together, hanging out in the hot tub, eating dinner, you get the idea. We did all of it together. So now with my own little ones in training (minus our 3 year old for now), the investment starts now to someday reach the goal of our own family ski trips.

Your Plan is King

You may be wondering "what does skiing have to do with the Market?" In order to reach my goal of family ski trips, I have determined it takes consistent, regular investment (time, money, planning) in their learning, patience, coaching, a long time perspective, and sticking to the plan. The same is true for investing and always keeping perspective of your goals.

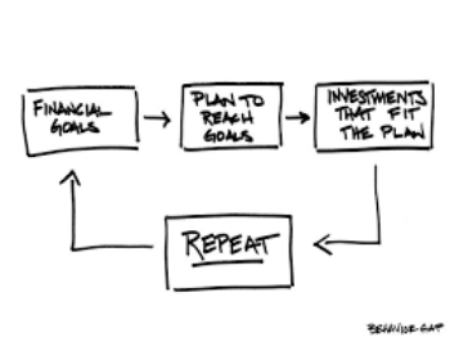

You have to focus on your financial plan.

The advisors at my firm and I often hear questions on what to do when the markets make headlines or when the pundits start beating their drums. The first question is: Do you have a financial plan? If no, the second question is: Then why not..? You should consider getting a financial plan. It is the road map to your future, providing consistent direction and strategy. If you have a financial plan, has it changed since the last market headline? Probably not, so re-focus on what your plan is. And turn off the TV, the pundits don't add any value.

Let Your Plan Keep You Focused

Determine your Goals and align them thru a strategic Financial Plan. This is in regards to your investments, insurance, college, taxes, legacy planning, you get the idea. It encompasses all areas. Remember the following:

Keep a long Time Horizon. My kids will not learn to ski on their first time out and your goals will not be reached overnight. For example, retirement takes years to attain with most people retiring in their late 60's. There are many different stages to successfully reaching a goal, seek to understand where you should be now.

Have Patience. Enough said? Maybe not. This is different than your time horizon. Do you fall down a lot when first learning to ski? It is realizing that it is not always easy to reach goals and unexpected things may challenge you. Your expectations may need to be adjusted depending on what happens in life and economic conditions you can't control like inflation/interest rates. There are no short cuts that work consistently. You can't repeatedly time or predict the markets so please don't try.

Determine what the "Right" Risk is for You. This is a highly individualized answer. Some people no matter how much skiing experience will ever be comfortable with a Double Black Diamond run. When thinking about your finances, Do you continually worry? If so, you may need to adjust your risk to a level you are more comfortable with. The stress you are causing yourself will not only decrease your enjoyment of life now but could possibly lead to health issues that may prevent you from enjoying your retirement goals to the fullest later.

Make Regular Investments. Few people can do something one time and be done. One time down the mountain or one investment contribution doesn't cut it. "Dollar Cost Averaging," or in other words, systematically and consistently investing money (think every pay check or every month) is a time-tested long term strategy used to help build wealth.

Seek Wise Counsel. I am a good skier but I know I am not the best to teach my kids, so I hire a professional ski instructor. Find a qualified and professional advisor or make sure your current "advisor" is the right one for you. A trusted advisor should always align themselves to your goals and what is in your best interests. If you don't know how to examine this, email me (luke.fields@raymondjames.com) and I will share the questions you should explore.

To Your Financial Success and Good Skiing,

Luke Fields, CFP®

Dollar-cost averaging cannot guarantee a profit or protect against a loss, and you should consider your financial ability to continue purchases through periods of low price levels. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Any opinions are those of Luke Fields and not necessarily those of RJFS or Raymond James. Expressions of opinion are as of this date and are subject to change without notice.

|

|

About Stewardship Cents

Stewardship Cents exists to Educate, Entertain and Enhance the financial wisdom of all who read it. Everyone needs to be wise with what has been entrusted to them and common sense can help us be good stewards of all that we have. Stewardship is a belief of responsible overseeing and protecting of important resources.

Luke Fields is Vice President of Foley & Foley Wealth Strategies, An Independent Firm, that has been based in Worthington, Ohio since 1981. A graduate from The Max M. Fisher College of Business at The Ohio State University, Luke is a CERTIFIED FINANCIAL PLANNER™, holding his Series 7, 66 and Ohio Life, Health and Variable Annuity Insurance licenses. He resides in Columbus, OH with his high school sweetheart, Beth and their three children. Luke is an active member of his church, serving in leadership and finances.

Follow additional insights and connect on LinkedIn, Facebook, his blog or Twitter. You can always reach him with comments or questions at: luke.fields@raymondjames.com.

Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC

|

|

|

|