Do Less, To Do More

Quarantined… we were counting the days. Now weeks. Most of us have slowed down, whether we like it or not.

No school, no spring break, no eating out, no sports (kids or professional), our days consist of working from home and more time with the family. Some have been laid off, some have tested positive for COVID-19, some have panicked, we have seen the stock market sell off, parents are becoming homeschool teachers. And all of us have felt the impact of this trial. In many parts of our lives, we are being forced to slow down from our busy schedules. However, there is hope in all these changes!

Slow Down and Get Better Results

Running has always been a stress reliever for me- now more than ever. When I trained at OSU, we did high intensity intervals for speed. Now, I train a bit slower which can be better. In training, if you hit certain target heart beats per minute (bpm) you can accomplish certain goals. For example, running at a slower pace and thus lower bpm, you can burn fat more efficiently. Doing less is doing more- slowing down can get better results.

I want to go fast in running, in life, work- and our schedules usually keep it that way. Although, in all we face currently, there is something freeing in our schedules being cleared. I call much of the last two weeks and likely many to come as “built in family time”. More breakfast, brunch, “linner” (to feed the tapeworms), dinner, family walks/workouts, games, exploring our yard and movie nights. I even predict there will be an explosion of births 9 months from now (not for us!). We are being taken back to what really matters.

We are being forced to focus on our faith, family, friends.

Is this easy? Nope- I am first to admit. Is it worth it and meaningful? Absolutely! I have seen neighbors in the past few weeks I never knew existed. People are walking their dogs, working out and chatting at a 6 foot minimum distance. Parents are out playing with their kids. Tackling my to do list has been nice. My neighbor nailed it when he said “this spring, yards will never have looked so good”. We all are choosing to “make lemonade”.

Don’t waste the opportunities to slow down and get better in this time of lockdown.

Things to consider in keeping active- spiritually, physically, mentally and socially….

Keep a schedule, develop a routine.

Pray.

Exercise.

This is a chance to read those books.

Work on your business not just work in your business. In what ways can you improve and better serve associates, clients, customers better?

Miss sports? Stream the greatest sporting events from YouTube for your kids to experience. We watched the 1998 NBA finals Bulls vs Jazz the other night.

Prepare yourself for a career change or new entrepreneurial adventure.

Spend more time with your loved ones, even if over facetime.

100 things to do during a pandemic

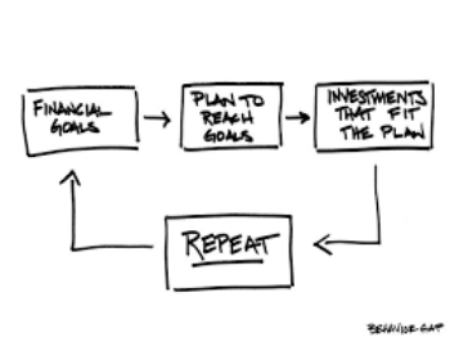

We continue to update financial plans and rebalance accounts as appropriate. What has your attention and is on your mind? Shoot me an email or give me a call, I am always available to discuss!

Luke Fields, CFP®